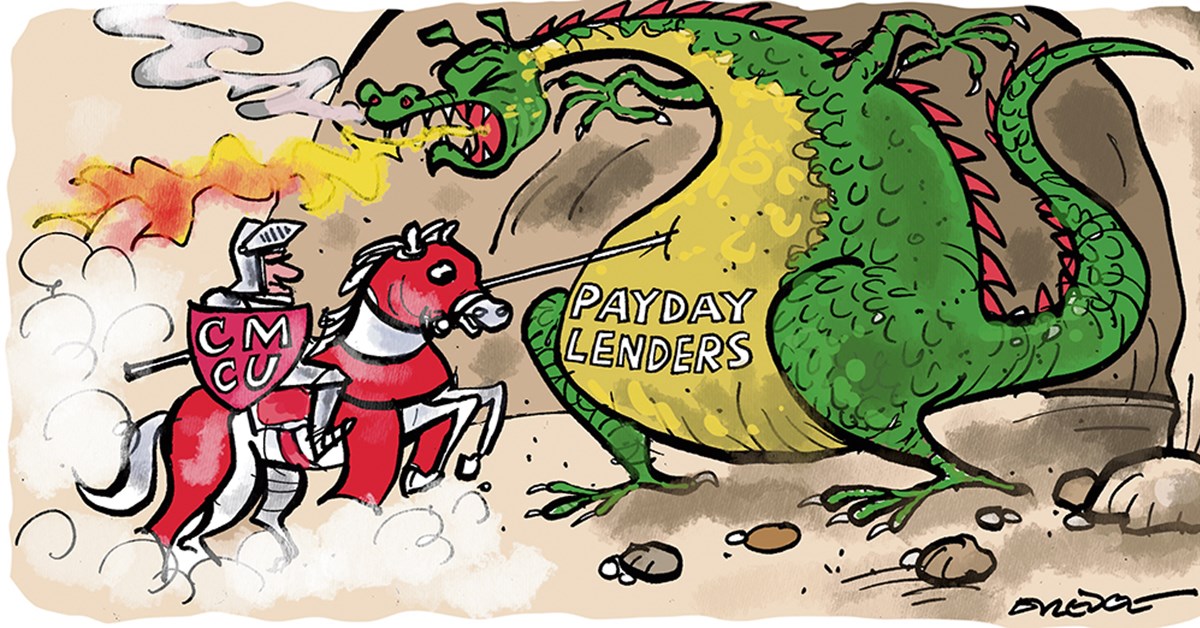

A FEW months after taking office, Archbishop Welby made headlines when he pledged to force payday lenders such as Wonga out of business by helping credit unions to compete with them.

His campaign gained momentum with the launch, ten years ago, of the Churches Mutual Credit Union: a joint project by several Christian denominations to give the church community a fairer financial choice. Over ten years, it has grown steadily, building trust and a reputation for being ethical and reliable.

In comparison with credit unions in Ireland or the United States, organisations that are old, large, and widely used, most credit unions in Britain are younger, work on a smaller scale, and are very much community-focused.

Churches Mutual began as a response to a real problem: exploitative practice in the lending market and an overall lack of financial resilience among a sector of the working population.

The idea was simple: to set up an alternative. Credit unions were an obvious choice of model, because they are about keeping financial value within communities. Credit unions offer fair regulated loans and savings, and they are accountable to members, not outside shareholders. This matters a great deal to people who have been preyed on by payday lenders or who struggle to obtain fair access to credit.

Churches Mutual focused on clergy, church workers, and others connected to congregations, or their associated schools and charities. Savers who place funds with the credit union to support the church community are its members, alongside borrowers who need affordable loans for the purchase of a new car, or even for ordinary things such as car repairs, household bills, or consolidating expensive debt.

THE credit-union sector has its challenges, of which the biggest has always been scale. Small credit unions struggle to afford modern systems, wide product ranges, or the compliance costs that come with regulation. This is why credit unions in Britain often cannot move as fast as big banks or lenders in other countries.

Technology is another challenge for credit unions. Members expect mobile access, quick payments, and easy account management. For many small credit unions, creating or buying good digital systems is just too expensive for them to do alone.

On top of that, the sector has been consolidating: there are fewer credit unions overall than there were 20 years ago, but more people are choosing to use them. This is a sign that the model is working, but it also shows the pressure that smaller unions are under either to grow or to merge.

Credit unions can get over these challenges by collaboration. A great example of such collaboration in solving tech problems is the recent joint project in which credit unions pooled resources to build a dedicated mobile app. Each credit union did not pay for an expensive bespoke system. Instead, the credit unions combined demand and worked with a single IT provider to build something tailor-made for their members. This allowed Churches Mutual to launch a modern app without shouldering the full development cost alone.

Regulation has also shifted in a helpful way: the Financial Services Act 2023 introduced new rules that allow credit unions to offer more products, such as secured car finance, mortgages, credit cards, and insurance.

Another structural idea borrowed from overseas is the Credit Union Service Organisation (CUSO) model. In places such as the US, credit unions set up shared companies that provide IT, payments, back-office functions, and specialist services. UK regulators are now looking at allowing similar structures here, which would help credit unions to share costs and expertise while keeping their mutual ownership.

POLITICALLY, there is momentum, too. The Labour Party has promised to grow the co-op and mutual sector, including credit unions, which could mean more support and faster expansion for community finance.

On a practical level, as credit unions build scale through partnerships, shared technology, and possible CUSOs, they will be able to offer better products, lower costs, and faster services.

Churches Mutual’s first decade shows how faith groups, shared purpose, and practical co-operation can create a trusted alternative to high-cost lenders and grow a sustainable financial service that gives people help when they need it.

Credit unions in Great Britain started later and smaller than in some other countries, but they are finding ways to adapt. Churches Mutual began to cut out predatory lenders, grew through denominational support, and used a collaborative approach with a technology firm to get a modern mobile app. With smarter regulation, political backing, and more shared solutions on the way, credit unions will keep being a vital and ethical option for people who need fair and community-focused financial services.

The Ven. Antony MacRow-Wood, a former Archdeacon of Dorset, is a founder and past president of the Churches Mutual Credit Union.