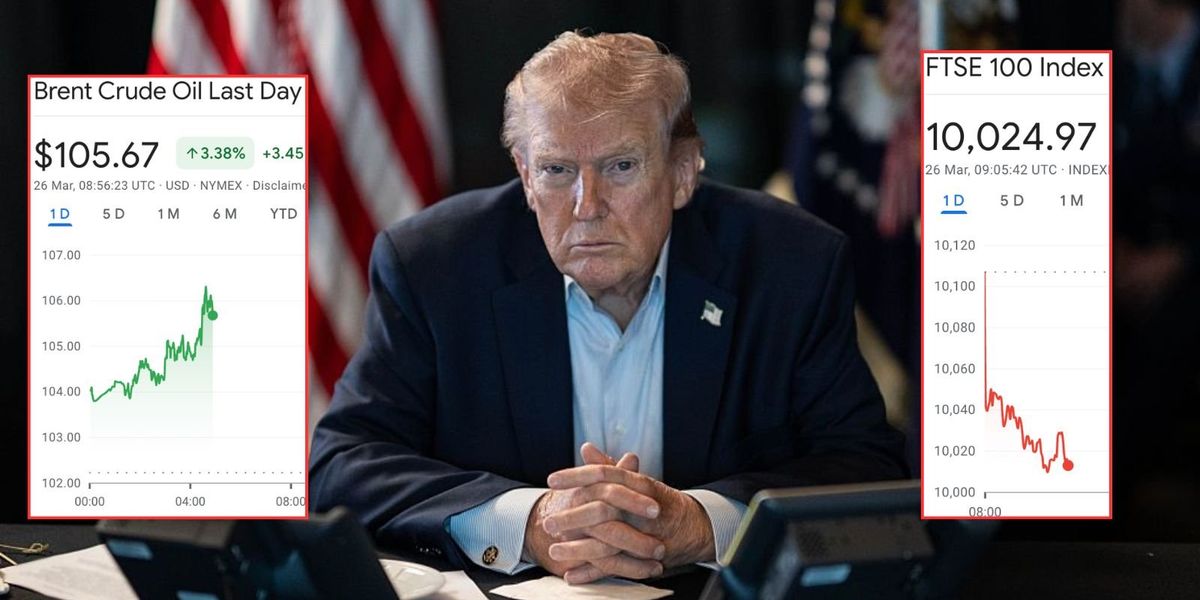

The Ftse 100 fell into negative territory on Thursday morning as oil prices climbed above $105 per barrel following Iran’s rejection of a US peace proposal.

Brent crude rose 2.6 per cent to $104.96, supported by disruption to shipping flows through the Strait of Hormuz and fading hopes of a ceasefire.

London’s blue-chip index dropped 0.6 per cent, falling 57.20 points to 10,049.64, reversing gains recorded over the previous two sessions.

Iran’s foreign minister said the country has “no intention of negotiating for now” with the United States, weakening investor optimism seen earlier in the week.

Deutsche Bank said President Donald Trump’s five-day deadline for postponing strikes against Iranian energy infrastructure is set to expire in just over 48 hours.

The bank added that thousands of US troops have reportedly been deployed to the region.

Next plc bucked the wider market trend, with shares rising more than six per cent after reporting what it described as an “exceptional” year.

Annual profits increased 14.5 per cent to £1.16billion, while sales rose 10.8 per cent to £7billion for the year ending in January.

Market volatility continues as Iran conflict drags on global economy

|

GETTY/GOOGLE FINANCE

The retailer said it has set aside £15million to cover additional costs linked to the Middle East conflict, including higher fuel and air freight expenses, assuming disruption continues for three months.

Chief executive Simon Wolfson said: “In the longer term, and if the conflict persists, the costs are likely to be reflected in higher prices to consumers and disruption to our supply chain, both of which are likely to suppress sales.”

Marks & Spencer shares also rose, gaining 4.6p to 338.4p following the update from Next.

Currys plc shares fell 10 per cent to 118.2p on the Ftse 250 after chief executive Alex Baldock said he would step down after eight years in the role.

Curry’s shares fell 10 per cent after its boss announced his departure

|

GettyMr Baldock is leaving to pursue a new opportunity, though the company has not disclosed further details.

Board chair Ian Dyson said: “Currys is very well positioned for future success with a strategy that is clearly working, great financial health and a very strong leadership team.”

Mr Baldock will remain in post while a successor is appointed.

The company said trading since January has met expectations, with adjusted pre-tax profit forecast between £180million and £190million for the year to May, representing growth of 11 to 17 per cent.

Co-op Group chief executive Shirine Khoury-Haq is also stepping down following a challenging year.

The mutual retailer reported an underlying pre-tax loss of £126million for the year to January three, compared with a £45million profit the previous year.

Revenues fell 2.3 per cent to £11billion, with a cyber attack accounting for a £285million impact on sales.

The leadership change follows reports in February of senior managers raising concerns about a “toxic” workplace environment.

Co-op said it stood by its culture and leadership following those claims.